Uber filed its latest earnings report last week, and as expected, the numbers looked as ugly as a 1970s AMC Gremlin with two flat tires. That said, the report did give an excellent example of one thing Calcbench loves to look at: adjusted earnings.

To be clear, adjusted earnings are a perfectly fine concept. One-time costs, stock grants, restructuring expenses, interest payments — those things happen, and a firm can argue that such costs don’t accurately reflect fundamental business activity. Hence the adjusted earnings.

Adjusted earnings are also perfectly fine to include in earnings releases and quarterly reports, so long as the firm provides a reconciliation from those adjusted earnings to actual earnings as defined under U.S. Generally Accepted Accounting Principles.

So nothing Uber ($UBER) reported for Q2 adjusted earnings is improper under SEC rules, but the company did take the idea of adjusted earnings on a wild ride.

First, the company presented a metric it calls “adjusted EBITDA.” That’s unusual right there because EBITDA itself is adjusted earnings — so adjusted EBITDA is what, exactly? Adjustment squared?

Uber says adjusted EBITDA is net income with an additional 13 adjustments for various expenses:

- (i) income (loss) from discontinued operations, net of income taxes,

- (ii) net income (loss) attributable to non-controlling interests, net of tax,

- (iii) provision for (benefit from) income taxes,

- (iv) income (loss) from equity method investments,

- (v) interest expense,

- (vi) other income (expense), net,

- (vii) depreciation and amortization,

- (viii) stock-based compensation expense,

- (ix) certain legal, tax, and regulatory reserve changes and settlements,

- (x) goodwill and asset impairments/loss on sale of assets,

- (xi) acquisition and financing related expenses,

- (xii) restructuring and related charges, and

- (xiii) other items not indicative of our ongoing operating performance, including COVID-19 response initiative related payments for financial assistance to drivers personally impacted by COVID-19.

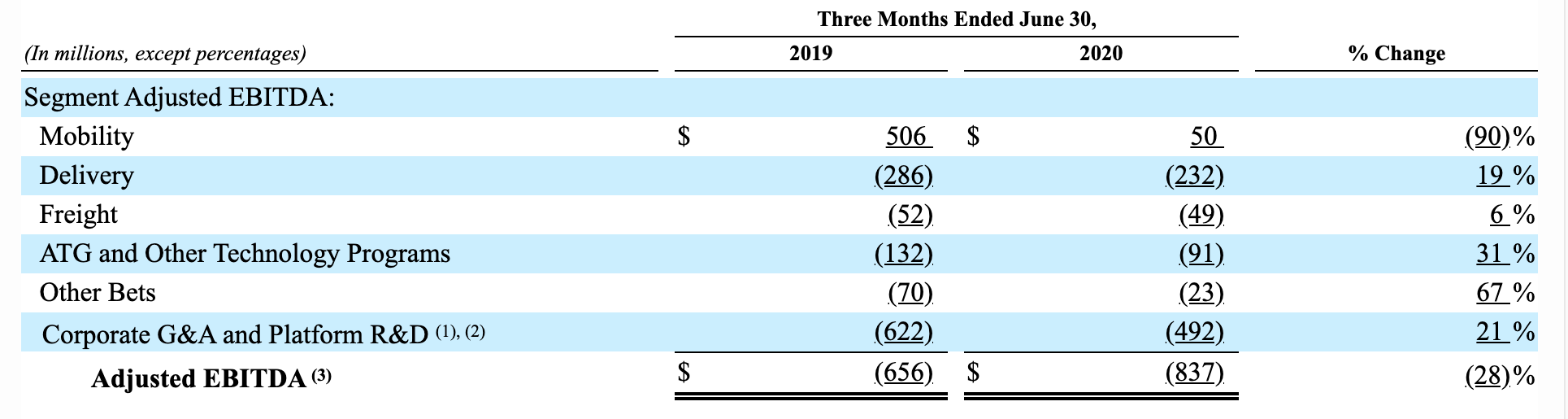

Uber also devised a metric it calls Segment Adjusted EBITDA, and we’ll just let Uber speak for itself on this one:

We define each segment’s Adjusted EBITDA as segment revenue less the following direct costs and expenses of that segment: (i) cost of revenue, exclusive of depreciation and amortization; (ii) operations and support; (iii) sales and marketing; (iv) research and development; and (v) general and administrative. Segment Adjusted EBITDA also reflects any applicable exclusions from Adjusted EBITDA.

So Segment Adjusted EBITDA is earnings before, well, everything, we guess. Uber does put that metric to use in a table that assigns Adjusted EBITDA to six operating segments. The tale it tells is that ride-share adjusted EBITDA plummeted, but the delivery segment grew, as did the other four segments. See said table, below.

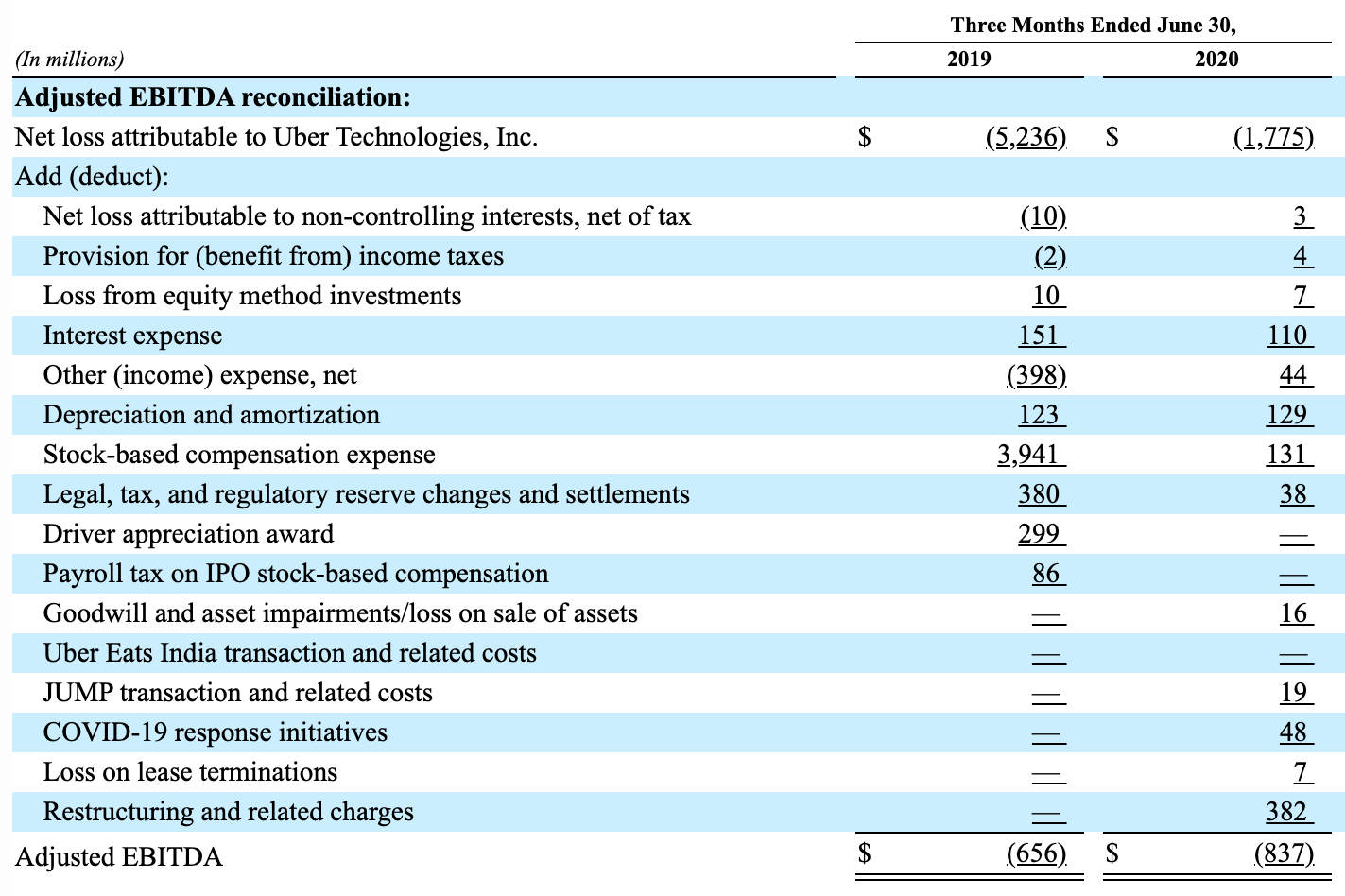

And finally, on the 18th page of Uber’s 18-page earnings release, we find the reconciliation from the $837 million loss in adjusted EBITDA to an actual loss of $1.77 billion for the second quarter. See Table 2, below.

The craziest part is that for all the pandemic havoc that Uber has endured this year, its many, many adjustments to EBITDA were even more beneficial to Uber last year, when its actual $5.2 billion loss (for one quarter!) was adjusted to an adjusted EBITDA loss of a mere $656 million. That’s mostly thanks to a stock-compensation expense of $3.9 billion last year that didn’t hit this year.