It’s Friday during earnings season, which means the Calcbench Earnings Tracker is back again with our latest look at Q3 earnings and how they compare to the year-ago period.

As devout readers of this blog know, we use the Earnings Tracker to collect financial disclosures as companies file their latest earnings releases with the Securities and Exchange Commission. We first turned on the tracker for Q3 2024 earnings several weeks ago; as of today we now have data on nearly 3,200 non-financial firms crunched and ready for your analysis.

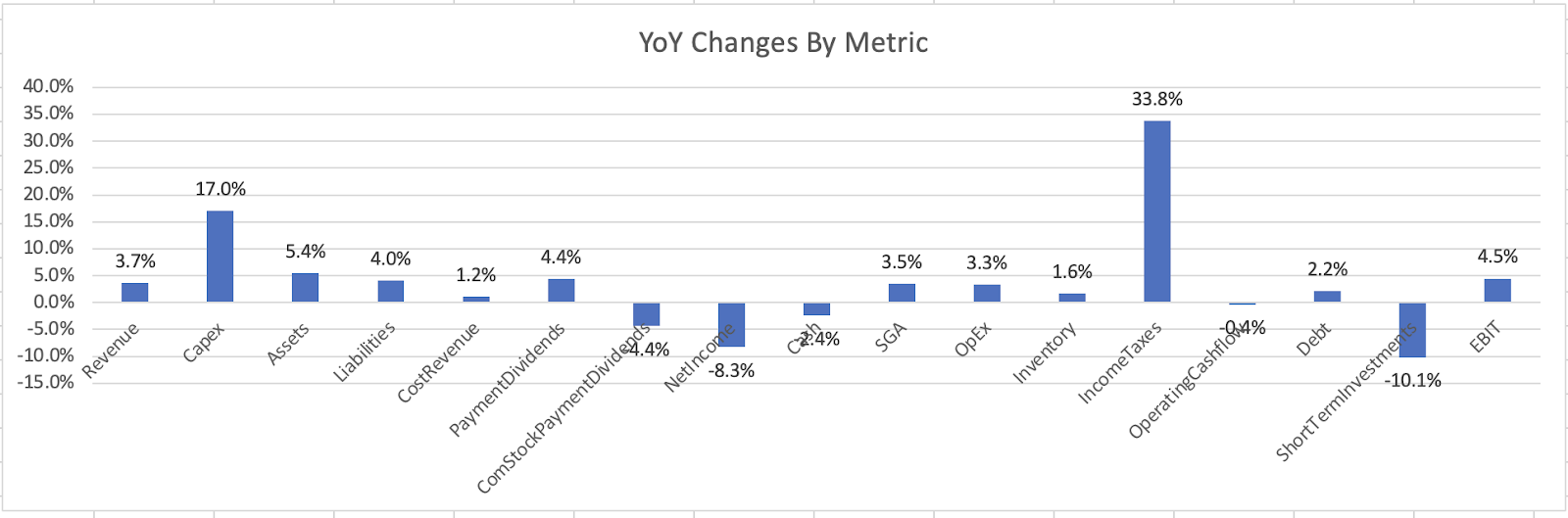

The headline performance numbers are in Figure 1, below.

As you can see, revenue is up 3.7 percent from the year-ago period, while net income is down 8.3 percent. We previously noted that the decline in net income was driven by two specific one-time items at Intel ($INTC) and Johnson & Johnson ($JNJ) that were so huge they skewed net income for the entire sample; strike those two, and net income for everyone else was actually up.

That still holds true this week. Net income for all 3,200 firms was collectively 8.3 percent lower than third-quarter 2023, but if you strike Intel and J&J, net income is actually up 2.1 percent.

Even more interesting, however, is that (net) capex spending number: up 17 percent from the year-earlier period. In theory that’s great news; it means that lots of companies are spending lots of money to buy equipment, build plants, install new technology, and do all sorts of other things to foster long-term economic growth.

So is that what’s really happening? As always, Calcbench dug into the data to find out.

Answer: no.

Concentration of Capex

First let’s look at the absolute numbers. Total capex spending reported so far for Q3 2024 is $322.1 billion. That’s an increase of $46.9 billion from the year-earlier amount, which was $275.2 billion.

But then we looked at the companies that reported the largest increases in capex spending. The 10 firms with the largest spending jumps reported a total increase of $49.1 billion — which is $3 billion more than the total increase for the whole sample group of 3,200 firms.

In other words, those big-spender firms accounted for all of the increase in capex spending, and then some. Among the other 3,190 firms in our sample, capex spending actually fell.

Figure 2, below, shows who those 10 big spenders actually are.

They are all tech companies, energy companies, and telecom companies. That’s it. Capex spending among all other companies, in all other industries, is collectively less this Q3 than it was one year ago.

What does that mean for economic growth in the future? We don’t know, but clearly an insight like this is worth keeping in mind as you run your own models and prepare for whatever earnings call is on your calendar. Calcbench gives you the information you need to ask better questions, and then find better answers.

Calcbench will continue to update our earnings tracker at the end of every week for the next few weeks, as quarterly reports flood into the database.

If Calcbench subscribers wish to get their hands on the template we use for this analysis, so you can conduct your own experiments at home, use this link to the file.

Please note that it will only work with an active Calcbench subscription. If you need an active subscription (and who doesn’t, really, when swift access to real-time data is so important?), contact us at us@calcbench.com.