Here’s a question any financial analyst could appreciate: what makes a good zombie?

Not the ‘Walking Dead’ type, of course, although that was a great show. We’re talking about zombie companies — firms that have such anemic growth and high debt costs that all they can afford to do every year is pay the interest on their debt. They have no other cash to invest in the business and get themselves growing briskly again, so they lurch from one fiscal year to the next, devoting all their operating income to debt service.

How many such companies exist these days? How long have they been zombies? And most importantly, how much longer could they exist as zombies?

That question has been on Calcbench’s mind since the Federal Reserve cut interest rates in September. If the Fed keeps cutting rates, it will get easier for firms to refinance that debt, especially if they racked up the debt in 2022 or 2023 when interest rates were high. Maybe zombies will come back into fashion.

To find the answers, we first searched all firms with more than $100 million in revenue in 2023 and then asked: how many of them had interest expense in 2023 that exceeded operating income?

We found nearly 800 firms that fit the profile, including some very large names: Bausch Health Cos. ($BHC), Carnival Corp. ($CCL), PG&E Corp. ($PCG), and National Steel ($SID), to name a few.

Walking Dead?

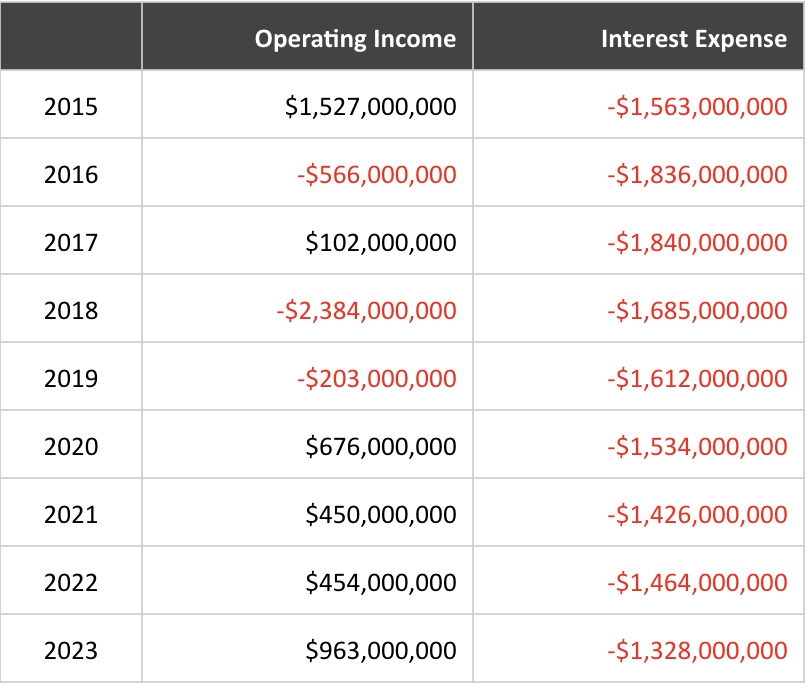

One company fitting the zombie profile is Bausch Health, a pharmaceutical company making various treatments for dermatology, gastrointestinal, and neurology disorders. Despite making at least $8 billion in annual revenue since 2015, Bausch’s annual interest expense has exceeded operating income the entire time. See Table 1, below.

What does zombie status mean for share price? Well, consider that Bausch shares hit an all-time high of $236 in July 2015. They have marched steadily downward ever since, and today trade at around $6.50 — and have been $6 to $8 for most of the last two years.

On the other hand, we also have companies like cruise giant Carnival Corp., where interest expense has exceeded operating income for three years running. But is the zombie label really fair for Carnival?

After all, the pandemic devastated cruise lines in 2020. They had to take on debt to survive, and reviving operations to pre-pandemic norms was always going to take years.

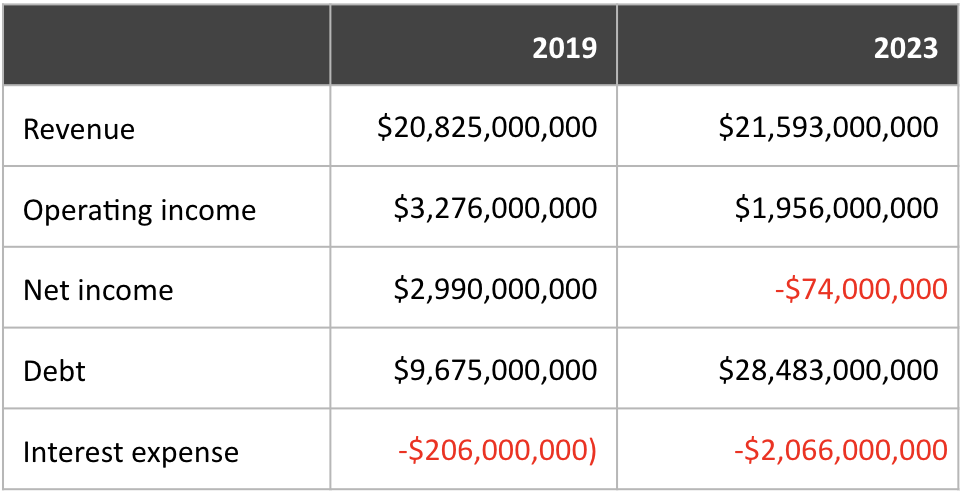

For example, compare these key disclosures from 2019 and 2023 in Table 2, below.

OK, the 2023 numbers are kinda gross, but there’s value there. Revenue is up, and operating income isn’t peanuts. This is a company that suffered a single, unforeseeable disruption and is living with the consequences — an economic heart attack, if you will, rather than the economic emphysema that has hobbled Bausch for years. Then again, both patients are still not in good health no matter what the cause.

Speaking of Debt…

You cannot analyze zombie companies without also considering the source of all their debt. After all, those debt levels drive the interest payments that push a company into zombie status — so where did that debt come from? How long will the payments last?

We can research those details in the debt disclosure footnote that companies file, which of course is readily available from the Calcbench Disclosures and Footnotes Query page. (Don’t forget our series on debt disclosures, published last year.)

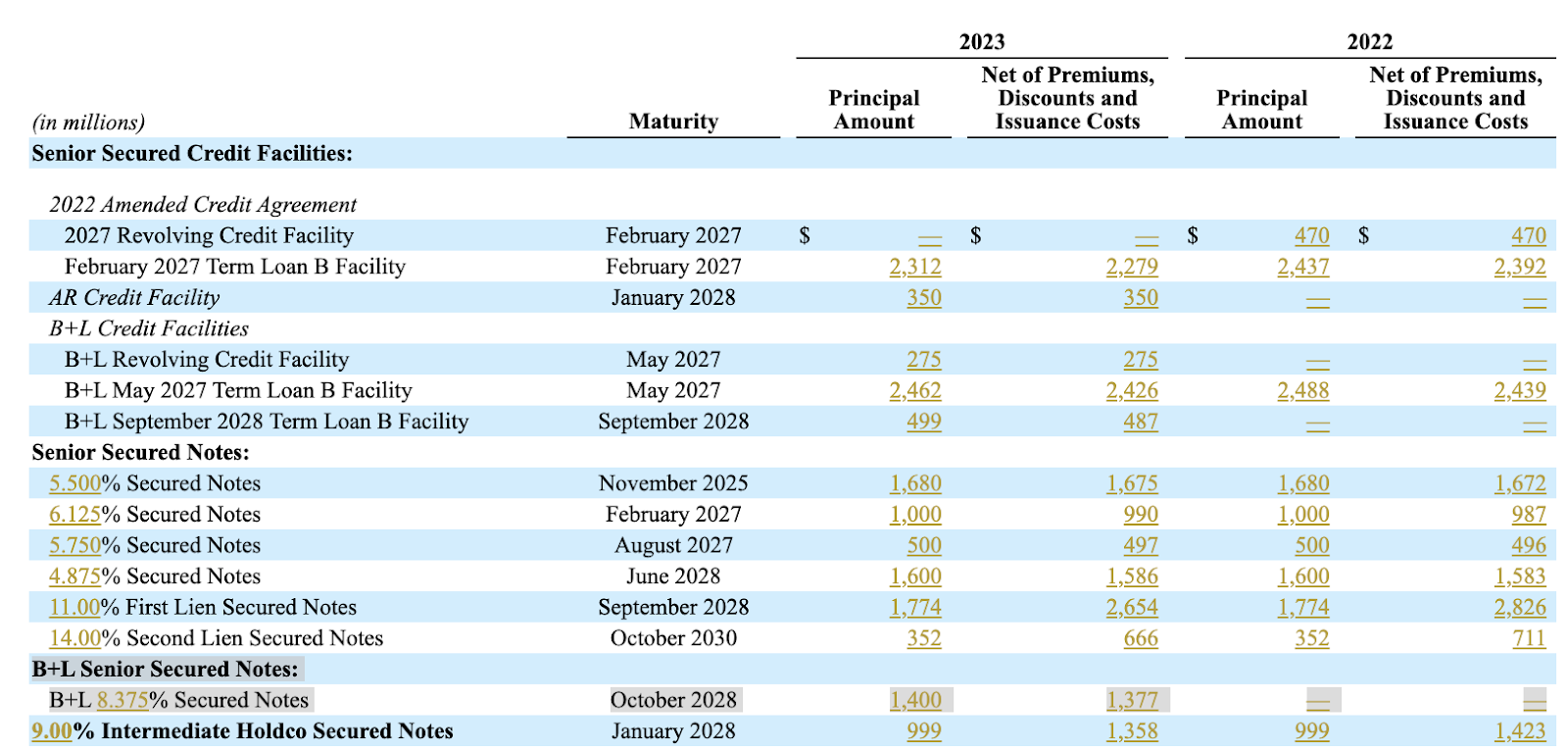

Let’s use the debt disclosure footnote from Bausch as an example. Tucked in the bottom of its table of debts is a new addition: a senior secured note obtained in 2023 for $1.4 billion, paying an 8.375 percent rate, due in October 2028. See Table 1, below; the new note is shaded gray.

OK, so Bausch took out $1.4 billion to do… what, exactly? We scrolled through the company’s 8-K filings (by selecting the “All Filings” at the top of the disclosures display) and started finding clues.

On June 30, 2023, Bausch disclosed that one of its subsidiaries was acquiring a business called Xiidra (plus a few other small businesses) from Novartis, for a total price of $2.5 billion. Then came this telling detail: Bausch “intends to finance the $1.75 billion upfront cash purchase price with new debt prior to closing.”

Ah ha! That’s why Bausch needed this $1.4 billion note!

We kept searching, and found another filing from Sept. 11, 2023, that disclosed the terms of that $1.4 billion note. The complete story is this, excerpted straight from the 8-K:

On June 30, 2023, Bausch + Lomb obtained commitments in respect of a $1,750 million 364-day bridge facility (the “Bridge Facility”), the proceeds of which, if such Bridge Facility were utilized, would have been used to finance all or a portion of the Acquisition (including related costs). In lieu of incurring indebtedness under the Bridge Facility amount on September 29, 2023, Bausch + Lomb incurred $1,900 million, in aggregate principal amount of indebtedness, consisting of: (i) $1,400 million aggregate principal amount of 8.375% Senior Secured Notes due October 2028 (the “October 2028 Secured Notes”) and (ii) $500 million in principal amount of new term B loans with a five-year term to maturity (the “September 2028 Term Facility”). Borrowings under the September 2028 Term Facility, together with a portion of the October 2028 Secured Notes, were used in connection with the Acquisition and effective September 29, 2023, the Bridge Facility was canceled.

One important question here is whether the $1.4 billion loan is callable — that is, whether Bausch could call the loan early and pay off the entire amount, to rid itself of that interest expense early. We found nothing that said Bausch can.

That’s an important point to ponder as the Federal Reserve starts cutting rates again. It’s possible that Bausch might be able to refinance this debt at a lower rate; but if the loan isn’t callable, that path is foreclosed. Bausch the zombie will need to lumber onward.