Most public companies file with the SEC both an earnings press release (through a Form 8-K) and an annual report (Form 10-K). The timing of the annual report is determined by the company’s filer status. For example, a large accelerated filer (a public float of more than $700 million) needs to file its 10-K within 60 days of the fiscal year end. The timing of the 8-K, however, is determined primarily by the company.

To file the 10-K the companies need their auditors’ approval, since the auditor’s letter is part of the filling. The earning press release does not require such approval.

Following up on our previous post on the topic, we wanted to take another look at the timing of both the earnings press release (the 8-K) and the annual report (the 10-K).

We examined all companies that have filed their 2017 annual report to date. We calculated average days from the fiscal year-end (FYE) to the filing of the 8-K and 10-K. We also calculate the percentage of time until the filing of the 8-K out of the total time until the filing of the 10-K. (For example, 100% would mean that both were filed on the same day).

2017 Annual 10-Ks Submitted |

||||

|---|---|---|---|---|

| Avg. Days FYE to 8K | Avg. Days 8K to 10K | Avg. Days FYE to 10K | Avg. Percent Time to 8K | |

| Large Accelerated Filer | 41.7 | 12.2 | 57.2 | 77.8% |

| Accelerated Filer | 53.5 | 13.9 | 70.3 | 80.4% |

| Non-Accelerated Filer | 54.8 | 10.8 | 79.7 | 84.1% |

| Smaller Reporting Company | 70.3 | 10.1 | 90.5 | 87.7% |

As can be seen from the table above, Large Accelerated Filers file their 10-K quicker than the other filers. That is no surprise; they are required to do so by law.

What is interesting is that, relatively, they file their earnings press release more quickly than other filers. That is, they publish the 8-K quickly (41 days on average after the FYE) and then spend more time working on their 10-K. The delay between the 8-K and 10-K is smaller (relatively) for the other (smaller) filer categories.

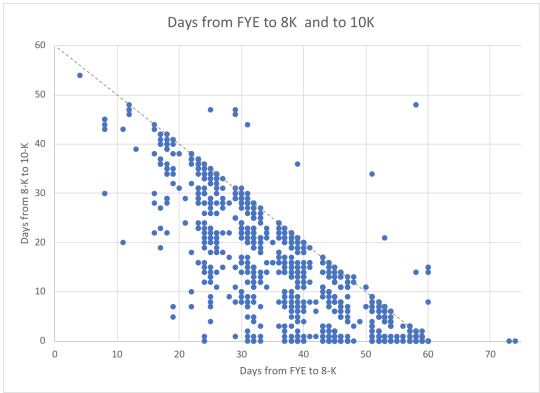

Closer look at Large Accelerated Filers

We wanted to take a closer look at the Large Accelerated Filers. We charted the number of days from the FYE to the 8-K and from the 8-K to the 10-K. All companies should have been below the diagonal line (file the 10-K within 60 days), and the vast majority did. In general, the closer the company is to the origin, the faster it files.

Conversely, the further from the origin (especially beyond the diagonal line), the longer it takes for them to file.

What is interesting though, is the timing of the 8-K relative to the 10-K. Companies on the X axis filed both the 8-K and 10-K on the same day, whereas companies higher in the chart had more of a delay.

We wanted to see whether the timing of the 10-K and delay between the 8-K and 10-K is associated with some other measures. We divided the Large Accelerated Filer to quartiles based on the days between the FYE and the filing of the 10-K.

Speed of 10-K Filing |

||

|---|---|---|

| Avg. %-age of time to 8K | Avg. Revenue (USD Billion) | |

| Very Fast | 81.4% | 11.6 |

| Fast | 76.4% | 8.2 |

| Slow | 76.0% | 7.0 |

| Very Slow | 77.7% | 3.1 |

We found that the companies that file the 10-K faster are larger and have less of a delay between the 8-K and the 10-K. This result may be a little surprising considering that larger companies are typically more complex and may require more time to prepare and audit the annual report. This result could, however, be driven by the market demand for information from the larger companies.